Real Estate Outlook 2026: From Global Trends to Growth Drivers in Vietnam

Entering 2026, the global real estate market is showing positive signs again, amidst a gradually stabilizing economy with new drivers, especially technology and artificial intelligence (AI).

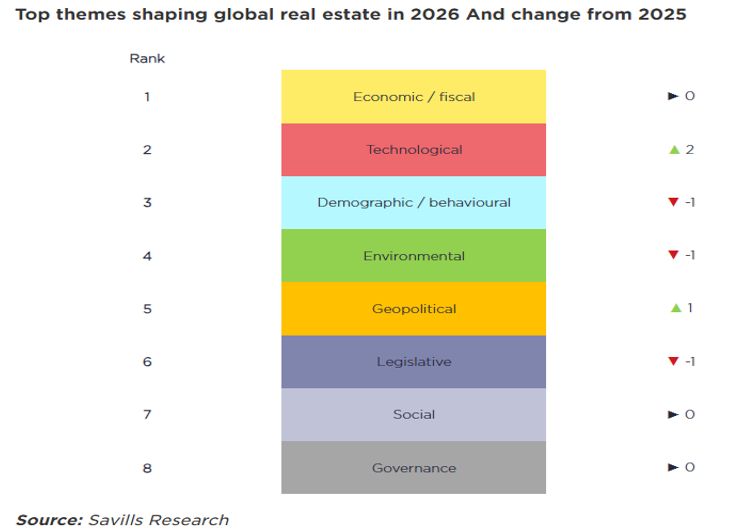

Trends shaping the global real estate market in 2026

According to Paul Tostevin, Director of Savills World Research, the economic outlook continues to be the biggest factor influencing the real estate market next year. The trend of interest rates gradually decreasing towards neutral levels is supporting both investment and rental demand. However, the new interest rate levels remain higher than before 2020, keeping capital costs high and putting pressure on the implementation of new projects.

However, as the market has somewhat adapted to the new interest rate environment, investment flows are returning more clearly, alongside a recovery in demand from leasing businesses . Savills forecasts that the total value of global real estate investment transactions could exceed $1 trillion in 2026, the highest level since 2022.

Technology, particularly AI, has risen to second place among the factors shaping the global real estate market. AI not only impacts the labor structure and office usage strategies of businesses, but also sparks a powerful wave of development in data centers and digital infrastructure. In the field of property management , AI drives intelligent operational, maintenance, and automation solutions, improving operational efficiency and optimizing costs in the long term.

Beyond technology, the human element remains central. A young population and rapid urbanization continue to drive growth in many emerging markets such as India, Saudi Arabia, and Vietnam, while global hubs like Dubai and Abu Dhabi benefit from migration and wealth accumulation. Changes in consumer behavior are also shaping demand for experiential retail, high-quality office space, and housing products suited to modern lifestyles.

Environmental pressures and regulatory frameworks related to emissions continue to increase. Along with this, new regulations on energy performance and climate reporting in Europe, Australia, and many other markets will drive up compliance costs and widen the gap between compliant and non-compliant assets.

Amidst volatile geopolitical conditions, trade tensions and protectionist policies continue to significantly impact industrial and logistics real estate. Trends such as supply chain diversification, “China+1,” and onshoring (manufacturing/services on-site) are driving warehousing demand in many emerging markets, including Southeast Asia.

Vietnam: Internal drivers in a new growth cycle

2025 marks a significant turning point for the Vietnamese economy, with GDP growth exceeding 8%, driven primarily by the industrial and high-tech sectors. This growth reflects the structural transformation of the economy, as Vietnam gradually moves away from a labor-intensive production model towards higher value-added industries.

Sectors such as electronics, semiconductors, renewable energy , and high-tech industries are attracting high-quality FDI, contributing to the upgrading of production value chains . Internationally, Vietnam is increasingly recognized as a strategic manufacturing hub in ASEAN, not only due to its cost advantages but also because of its stability, adaptability, and extensive network of trade agreements.

Mr. Matthew Powell, Director of Savills Hanoi

According to Matthew Powell, Director of Savills Hanoi, this shift creates a solid foundation for the real estate market, which has already seen a clear recovery since the end of 2025. Entering 2026, industrial and residential real estate are predicted to continue leading the market.

In the industrial segment, demand is focused on industrial land in key manufacturing centers such as Bac Ninh, Hai Phong, Binh Duong, and Dong Nai; along with the strong development of ready-built factories, modern warehouses, and logistics zones connected to seaports, airports, and highway systems.

In the housing segment, products serving genuine housing needs are considered a sustainable growth driver, including mid-range apartments, affordable housing, and satellite urban development projects along new infrastructure corridors. These segments directly benefit from urbanization and the increasing workforce in industrial centers.

However, rapid growth also poses the risk of forming localized "hot spots," especially in large cities where housing prices tend to rise faster than incomes. Risk management requires coordination between transparent land policies, expanding the supply of affordable housing, controlling credit, and directing development towards satellite areas.

From a policy perspective, the implementation of resolutions on private sector development, especially Resolution 68, is opening up significant opportunities for domestic businesses to participate more deeply in large-scale infrastructure and industrial park projects. Reforms in administrative procedures, land access, and diversification of capital sources are expected to help unleash private resources, enhance project implementation capacity, and strengthen investor confidence.

To maintain sustainable growth in 2026 and beyond, Vietnam needs to continue attracting high-quality FDI, especially in the green manufacturing sector. This requires a clear policy framework for green development, selective incentives, strong investment in renewable energy, green industrial park infrastructure , and improved human resource quality.

Communicated by An Huy Group

Related News

The income ceiling for purchasing social housing will officially be raised to 25 million VND/month from April 7, 2026.

(Chinhphu.vn) - In Decree No. 136/2026/ND-CP, the Government stipulates raising the income ceiling for individuals purchasing social housing to 25 million VND/month.

View Details

From July 1st, 2026, what will be the interest rate for loans to purchase social housing for people under 35 years old?

Given the high interest rates on commercial home loans, the preferential credit policy effective from July 1, 2026, is expected to help young people reduce financial pressure and increase their access to social housing. So, from July 1, 2026, what will be the interest rate for loans to purchase social housing for those under 35 years old?

View Details

Officially adding a priority group for purchasing social housing.

From July 1, 2026, people with two or more children will be prioritized to buy, lease-to-own, or rent social housing according to the new regulations.

View Details

From July 1st, customers under 35 years old at Vietcombank, Agribank, BIDV, VietinBank, MB, etc., will all receive good news.

From July 1st to December 31st, 2026, people under 35 years old who borrow to buy social housing will enjoy preferential interest rates.

View Details

Announcement of the revised Tay Ninh 2030 planning: New administrative center in Duc Hoa - Hau Nghia.

According to the plan, the Tay Ninh Provincial Political and Administrative Center will be located in the northern area of Duc Hoa - Hau Nghia urban area. The specific construction location will be studied and proposed based on ensuring requirements for spatial development, connectivity, and synchronization of technical infrastructure and transportation systems of the province and the Southeast region.

View Details

5 satellite cities help alleviate congestion in Ho Chi Minh City center.

Ho Chi Minh City - Thu Duc City is a highly interactive and innovative urban area in the East; Can Gio is a coastal ecological urban area; the southern urban area has Phu My Hung as its center; the southwestern urban area (Binh Chanh) is a gateway to the Mekong Delta; and the northwestern urban area is a gateway connecting to Binh Duong, Tay Ninh, and Cambodia.

View Details

The important role of 5 satellite cities for Ho Chi Minh City.

Ho Chi Minh City will develop five satellite cities to alleviate population density and address a range of related issues such as traffic, pollution, and quality of life.

View Details

Ho Chi Minh City develops satellite cities.

The satellite cities in Ho Chi Minh City that will be formed after 2030 will not follow the mechanical process of upgrading districts to cities, but rather will be independent urban clusters connected via urban rail.

View Details

Chairman of Ho Chi Minh City: Develop 5 satellite cities based on the TOD model.

Besides Thu Duc City, Ho Chi Minh City is also developing four other satellite cities associated with the Transport-Oriented Development (TOD) model, including Can Gio, the South, Southwest, and Northwest areas.

View Details

The legal framework expands opportunities for overseas Vietnamese to invest in real estate in Vietnam.

According to data from the State Bank of Vietnam – Regional Branch 2, in the first nine months of 2025, Ho Chi Minh City recorded approximately US$7.94 billion in remittances, accounting for nearly 60% of the total remittances nationwide. The main sources of remittances were Asia (50%) and the Americas (30%).

View Details

Fluctuations in capital costs and the adaptation challenge for homebuyers.

The upward adjustment in mortgage interest rates is making many buyers and investors more cautious in making financial decisions. According to experts, this is not a negative signal for the real estate market, but rather a factor that promotes a more sustainable adjustment process.

View Details

With abundant supply, the real estate market reflects a trend of diversified capital flows.

The widespread increase in supply, with a growing diversity of product types and price ranges, gives buyers more choices, while also making the trend towards selectivity more pronounced.

View Details

Understanding the property identification code applicable from March 1st.

From March 1st, 2026, electronic property identification codes will be issued to each property. So what do people need to know about the property identification codes that will be applied from March 1st?

View Details

Tay Ninh will relocate its new administrative and political center to Duc Hoa - Hau Nghia.

The Chairman of the People's Committee of Tay Ninh province, Le Van Han, has just signed and issued the revised Provincial Planning for the period 2021–2030, with a vision to 2050, aiming to shape a new development space and take advantage of its location bordering Ho Chi Minh City, Dong Nai, Dong Thap, and Cambodia.

View Details

Determined to increase market transparency and "close the gaps" in real estate transactions.

Recently, Prime Minister Pham Minh Chinh directed the urgent pilot operation of a cryptocurrency exchange platform, and simultaneously established a State-managed Real Estate and Land Use Rights Transaction Center, with the goal of implementation in February 2026. This is a strong move, clearly demonstrating the Government's determination to restructure and increase transparency in the real estate market…

View Details

Expedite the finalization of documents for establishing a Real Estate and Land Use Rights Transaction Center; strictly control speculative real estate credit.

(Chinhphu.vn) - Prime Minister Pham Minh Chinh directed the urgent completion of the dossier for the establishment of a Real Estate and Land Use Rights Transaction Center; and requested strict control over speculative real estate credit, focusing on the actual housing needs of the people.

View Details

What Does the World Say About Vietnam's Real Estate Market?

In the context of Vietnam's real estate market moving beyond a period of profound adjustment and facing the imperative for comprehensive restructuring, the narrative of sustainable development is no longer merely a guiding slogan but has become a practical challenge of existential importance.

View Details

Tay Ninh Master Plan 2030: Duc Hoa – Hau Nghia OFFICIALLY Approved as Provincial Political and Administrative Center

At the 9th Session (specialized session) of the 10th Legislature, the People's Council of Tay Ninh Province officially adopted a Resolution on Adjusting the Tay Ninh Provincial Master Plan for the period 2021-2030, with a vision to 2050. The most significant highlight of this revised master plan is the designation of the Duc Hoa – Hau Nghia urban cluster as the new political and administrative center of the province, marking a strong transformation in the organization of development space following provincial consolidation.

View Details

Sharp increases in land plot prices are observed, and the market is projected to witness an explosion of supply in 2026.

Land plot prices are set to keep increasing through 2025, as demand clearly improves and new supply is anticipated to make a strong comeback in 2026.

View Details

Legal Transparency Becomes An Huy Group's Competitive Advantage

Recently, An Huy Group distinguished itself by successfully meeting the stringent selection criteria to receive the "Top 10 Distinguished Legally Transparent Real Estate Enterprises" award.

View Details

An Huy Group was honored as one of the “Top 10 Real Estate Enterprises with Outstanding Legal Transparency.”

Recently, at the announcement ceremony of the “Asia-Pacific Excellent Brand 2025”, Cong ty Dia oc An Huy (An Huy Group) successfully surpassed stringent evaluation criteria to receive the award “Top 10 Real Estate Enterprises with Outstanding Legal Transparency.”

View Details

An Huy Group was honored as one of the “Top 10 Real Estate Enterprises with Outstanding Legal Transparency.”

Recently, at the announcement ceremony of the “Asia-Pacific Outstanding Brand 2025”, Cong ty Dia oc An Huy (An Huy Group) successfully met and surpassed stringent evaluation criteria to receive the award “Top 10 Real Estate Enterprises with Outstanding Legal Transparency.”

View Details

Announcement of Report: Real Estate in Tay Ninh Province After the Merger – Synergistic Strengths and Breakthrough Opportunities

On November 6, 2025, the Vietnam Real Estate Research Institute (VIRES) officially released the market report: "Real Estate in Tay Ninh Province After the Merger – Synergistic Strengths and Breakthrough Opportunities."

View Details

Pickleball Cup An Huy 2025 – 1st Edition: Spreading the Spirit of Sports, Connection, and Sharing

At noon on November 8, 2025, the atmosphere at the four Pickleball courts in An Huy My Viet Urban Area (Rung Sen Hamlet, Duc Lap Commune, Tay Ninh Province – formerly part of Duc Hoa District, Long An Province) became lively and exciting as the 1st An Huy Pickleball Cup – 2025 officially kicked off.

View Details

Upcoming Market Report Release: "Tay Ninh Province Real Estate After the Merger – Synergistic Strength and Breakthrough Opportunities"

Scheduled for November 6, 2025, the Vietnam Real Estate Research Institute, in collaboration with Vietnam Real Estate Online Magazine, will release the Market Report: "Tay Ninh Province Real Estate After the Merger – Synergistic Strength and Breakthrough Opportunities."

View Details

The Steadfast Advancement of An Huy Group with the Honor of “Asia’s Leading Trusted Brand 2025”

The title “Asia’s Leading Trusted Brand 2025,” recently awarded to An Huy Group, marks a proud milestone that recognizes the company’s more than two decades of steadfast effort in affirming the stature of a Vietnamese brand.

View Details

The An Huy My Viet Project wins the Best Township Heritage Landscape Design Vietnam 2024 award.

At the DOT Property Vietnam Awards 2024 ceremony held on September 26, 2024, the An Huy My Viet Project, developed by An Huy Group, excelled in winning the “Best Township Heritage Landscape Design Vietnam 2024” award.

View Details

BIDV Bank and An Huy Group Sign Credit Financing Partnership Agreement

On September 6, 2024, the Bank for Investment and Development of Vietnam (BIDV) and An Huy Real Estate Joint Stock Company (An Huy Group) held a signing ceremony to establish a partnership supporting customers in obtaining financing when purchasing real estate products at the An Huy My Viet Urban Area.

View Details

Notice: Warning Against Fraudulent Use of the An Huy Group and An Huy My Viet Brands

Currently, An Huy Group is developing the An Huy My Viet Urban Area in My Hanh Bac Commune, Duc Hoa District, Long An Province. The An Huy My Viet Project has officially commenced construction and is being implemented in strict compliance with current real estate investment laws and regulations.

View Details